Feb 19, 2026

The Five Key Risks of Document Fraud: A Front-Line Threat

In the fast-moving world of financial services, handling documents might seem like a routine tick-box exercise, but it is a critical step that provides a holistic view of borrower income and helps validate details across payments or insurance.

Ensuring the correct risk controls are in place will allow lenders or insurers to use these documents with confidence. This article outlines five key risks of document fraud and why these should matter to any institution processing documents and images at scale.

Regulatory Risk

Regulators around the world have increasingly homed in on document-based fraud as an enabler to financial crime. In Australia, AUSTRAC, the AML/CTF regulator, has warned that non-bank lenders face a medium risk of money-laundering and terrorism financing, with fake documents in loan applications being a major concern.

Both the Australian Prudential Regulation Authority (APRA) and the Australian Securities & Investments Commission (ASIC) are also increasingly zeroing in on how lenders handle documentation in loan-origination and credit-assessment processes. For example, ASIC’s guidance on responsible lending highlights the importance of verifying a borrower’s financial situation and correctly recording assessments to prevent unsuitable credit contracts.

In the United States, regulators have taken a similarly firm stance. The Federal Deposit Insurance Corporation (FDIC) has warned that falsified income documents, doctored bank statements and synthetic identities are now central enablers of both credit fraud and money-laundering.

The Office of the Controller of the Currency (OCC) has also stressed that poor documentation standards undermine a bank’s ability to demonstrate “sound underwriting and effective BSA/AML compliance,” noting that inconsistent verification practices expose institutions to heightened supervisory scrutiny.

Together, these signal that inadequate document fraud controls are no longer treated as administrative oversights.

The message is clear: reviewing supporting documents is no longer just a back-office concern…it’s a potential regulatory red-flag.

“From falsified income documents to fabricated bank statements, document fraud is a key enabler of financial crime.”

Sean Quagliani, CEO Fortiro

Reputational Risk

When document fraud goes undetected, it not only poses a risk to the bottom line but also to customer trust.

In 2025, one of Australia’s biggest banks was allegedly defrauded of AU$150million in an incident involving fraudulent documents used for loan applications. New South Wales Police later described the incident as ‘violating the bank’s position of trust’.

In the UK, the official Crime Survey for England & Wales estimated around 3.9 million fraud incidents in the year ending September 2024 – a 19% increase. These large numbers mean consumers are already alert to fraud issues; when a business is publicly found weak in verifying documents, the brand damage can be swift and enduring. This exemplifies how reputational fallout can follow operational lapses.

Risk of Fraud Losses

Document fraud is not just about compliance and optics. There are real financial losses at stake. In Canada, it was noted only 5–10% of fraud incidents are reported and that impersonation fraud has pushed reported losses beyond CAD $2 billion since 2021.

In the UK, KPMG has reported that while high-value fraud cases decreased in 2024, the volume of total fraud cases increased, and total value reported via courts for cases >£100k was £453.2 million in 2024.

These statistics underscore that when a fraudster submits a fake paystub or doctored bank statement, the institution may suffer non-payment, charge-back, or remediation costs. Those losses can mount quickly.

At Fortiro, we prevent on average $25m in fraud losses per month for our customers by detecting fraudulent documents and images.

Reliability Risk

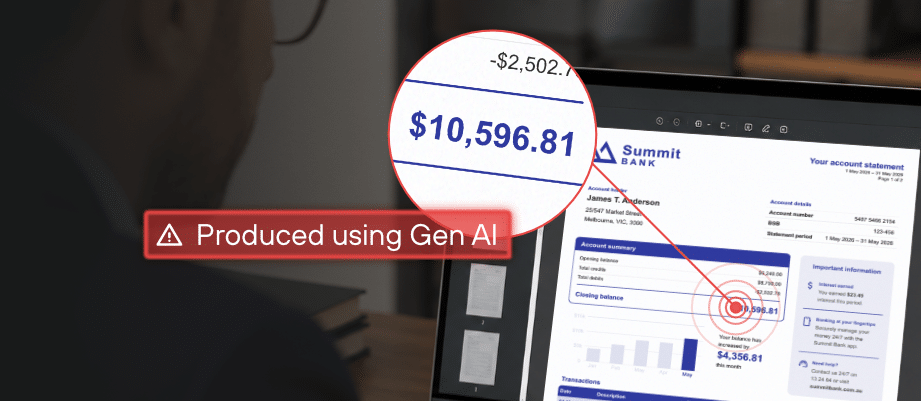

The processes that organisations put in place to use documents to validate critical information, such as income, are only as good as the documents themselves. In Australia, recent media commentary has highlighted that document fraud tactics are evolving (including AI-assisted falsification of payslips, bank statements and synthetic identities).

In the UK, one fraud prevention service reported 421,000 cases filed to the National Fraud Database in 2024 – the highest number on record and a 13% increase – suggesting fraudsters are increasingly using false applications and identity/document manipulation.

The figures suggest that manual or legacy verification processes are increasingly unreliable in keeping pace, and the document‐handling workflow can become a weak link. If an organization’s process is unable to consistently identify manipulated documents, then that organisation is exposed.

Human error

Even with solid systems in place, humans will always be part of the document chain: uploading, reviewing, verifying, approving. Mistakes happen – typos, misreads, oversight, fatigue.

It goes without saying that human reviews at scale are likely to have a higher margin for error. For instance, automating 95% of reviews and having humans focus on flagged documents will only allow for more effective and efficient processing.

Reported increases in volumes of fraud imply that human reviewers are under increased pressure, which heightens the chance that fraudulent documents slip through. Together, rising fraud sophistication + high volume + human error = a potent combination of risk.

In a world where AI can replicate documents and images with ease and at scale, being able to differentiate between fake documents and genuine, authentic documents is more important than ever.

Summary

Document fraud has moved from the back office to the front line of risk. Falsified payslips/pay stubs, edited bank statements and AI-generated documents now sit behind a growing share of credit, payments and insurance decisions.

Regulators in Australia, the US, Canada and the UK are responding by treating weak document controls as a compliance failure, not a clerical error. At the same time, fraud volumes are rising and human reviewers are under pressure, making manual checks increasingly unreliable. The result is a dangerous gap where bad documents can drive bad decisions, undermine AML programs and create real financial losses.

In today’s environment, being able to prove a document is genuine is no longer optional. It is core to protecting revenue, reputation and regulatory standing. Because when a document fails, the consequences ripple far beyond the page.

Get a demo today

Get a demo of Fortiro’s income document verification platform to see how it can help you.