Mar 5, 2026

Loan Application Fraud: a Hidden AML Risk?

When an applicant submits falsified payslips or edited bank statements to secure a loan, that credit facility can become a clean on-ramp for dirty money. What looks like “income stretching” or “staged wages” is often something very different. In other words, weak document and income verification controls at origination do not just create credit risk. They can turn your loan book into an accidental laundromat.

If your AML program is focused only on transaction monitoring and sanctions checks, you are likely missing a key enabler: the documents that get the money in the door in the first place. The only way to see these crimes clearly is to double-check the documents you are relying on.

Laundering often begins at origination. Miss the document fraud and every control that follows is working with the wrong information.

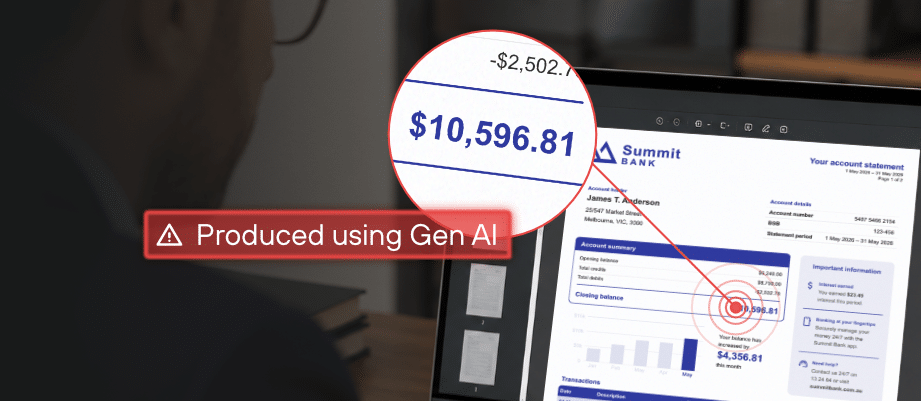

Around the world, when it comes to consumer credit, first-party fraud and “side hustle” income inflation are now routine. Applicants tweak their incomes through doctored paystubs, screenshots, and edited bank PDF statements.

At the other end of the spectrum, organised groups industrialise the same methods at scale, recycling templates and datasets across many identities and lenders. These are not minor applicant behaviours or edge cases. They quietly distort affordability assessments and contaminate the data that risk models depend on.

The AML connection is direct. Loan-based laundering is now a recognised typology: criminals obtain a loan with falsified documentation, make several regular repayments, and then pay out, default, or in asset backed products, even sell the goods. From the outside, the funds look like legitimate credit proceeds that have moved through a regulated financial institution. False documentation is what makes this possible. If the origin point is weak, the most sophisticated downstream AML controls are working with tainted assumptions.

Sector pressures are making this worse. Brokers are judged on turnaround times. Challenger and non-bank lenders sell speed as their core value proposition. Manual reviewers are stuck playing catch-up, often checking documents after approval or only when something “feels wrong.” In that environment, subtle fraud that sits just inside policy settings slips through unnoticed, even as aggregate exposure grows. This is where automated document forensics becomes an AML control, not just a fraud tool.

As one Chief Risk Officer from a prominent Non-Bank Lender shared:

“We see a very tight relationship between fraud and AML. Every time a new customer approaches our business, we are building a scorecard and a picture of that customer, which can lead us directly into Enhanced Customer Due Diligence (ECDD). And for one customer, it could be tampered documents; but for another customer, it could be something totally different.

The main thing is that we bring together many datapoints to build this picture as quickly and as accurately as we can. And I think this is the expectation of the regulator and society in general.”

Fortiro Protect analyses digital document data, image and PDF forensics, metadata, and visual appearance in a consistent, scalable way. It can detect overlay artefacts that suggest editing, AI-generated documents, rounded or inconsistent income figures, cloned structures reused across different applications, and metadata that does not align with the claimed source of a file. These signals do not replace human judgement, but they radically change which documents get a second look.

The market is already shifting toward independent data sources and automated document forensics. Regulators are paying closer attention to how lenders verify income and assess suitability. Not investing in this capability is no longer only an operational choice. It is a regulatory and balance sheet exposure, with a real risk that your institution is seen to profit from the proceeds of crime.

It is time to treat document validation as a core pillar of AML, not simply an administrative step in loan origination.

Talk to Fortiro today about how we can help you put an automated document and image fraud system in place that strengthens both your credit and AML defences.

Get a demo today

Get a demo of Fortiro’s income document verification platform to see how it can help you.