Sep 24, 2025

Protecting Your Business Against Application Fraud in 2025: Strategic Imperatives Across Industries

In 2025, application fraud continues to pose a substantial risk to businesses across diverse sectors. The increasing sophistication of fraudulent tactics, driven by advancements in technology, necessitates a proactive and multifaceted approach to mitigation.

This analysis outlines nine key strategies for safeguarding your organisation against application fraud, tailored to the specific challenges faced by various industries. These strategies are not merely tactical responses but strategic imperatives for maintaining business integrity and customer trust.

1. Establishing Robust Identity Verification Protocols:

The foundation of fraud prevention lies in verifying the true identity of applicants. Advanced Identity Verification Solutions are crucial, moving beyond basic checks to incorporate:

- AI-Powered Biometrics: Leveraging facial recognition, fingerprint scanning, and voice analysis to confirm applicant identity against government-issued IDs.

- Liveness Detection: Employing technologies that detect “spoofing” attempts, ensuring the presence of a live individual during the verification process.

- Deep Fake Detection: Utilising sophisticated algorithms to identify manipulated videos or images used to impersonate individuals.

- Pattern Recognition: Identifying subtle inconsistencies in applicant data that suggest synthetic identity creation.

Industry Application: In the financial services sector, particularly banking, these tools can effectively prevent fraudulent loan applications and new accounts based on fabricated identities or stolen credentials. Telecommunications companies can prevent the fraudulent opening of accounts for high-value devices by effectively detecting synthetic identities.

2. Implementing Behavioural Analytics for Anomaly Detection:

Behavioural analytics offers a powerful means of identifying suspicious patterns during the application process. By monitoring user interactions, such as:

- Typing Speed and Cadence: Detecting unusually rapid or robotic form-filling behaviour indicative of automated attacks.

- Navigation Patterns: Identifying inconsistent or illogical navigation through the application interface.

- Data Entry Discrepancies: Flagging inconsistencies between entered data and previously provided information.

Industry Application: E-commerce platforms can employ behavioural analytics to identify and block bot-generated accounts used for fraudulent purchases or promotional abuse.

3. Integrating Cross-Channel Fraud Detection Systems:

Fraudsters often exploit inconsistencies between different communication channels. A robust defence requires integrating fraud detection across all touchpoints, including:

- Web Portals: Monitoring online applications and account access.

- Mobile Applications: Analysing mobile user behaviour and device characteristics.

- Call Centres: Verifying information provided during phone interactions.

Industry Application: Healthcare providers can utilise cross-channel detection to identify discrepancies in patient information or insurance claims submitted through various platforms, mitigating insurance fraud.

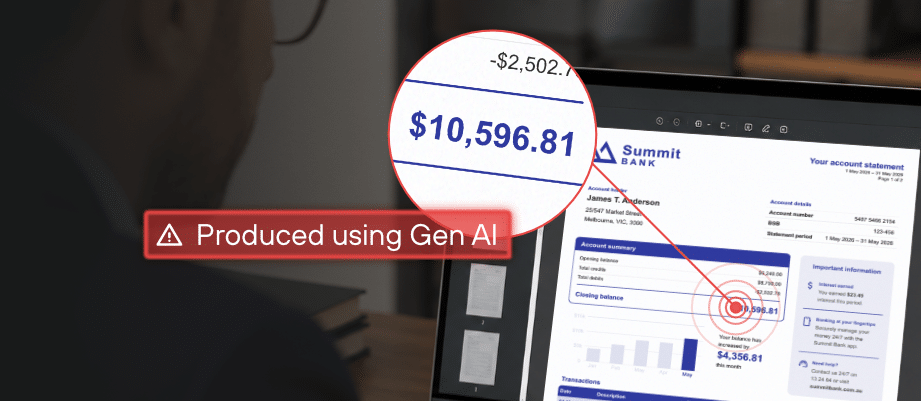

4. Utilising Advanced Document Fraud Detection:

The submission of falsified documents is a common tactic in application fraud. Advanced document analysis tools can:

- Verify Document Authenticity: Detecting tampering, forgeries, and inconsistencies in submitted documents like pay stubs, IDs, and utility bills.

- Extract and Validate Data: Automating data extraction from documents and cross-referencing it with other data sources.

Industry Application: Property management firms can use these tools to validate tenant applications, preventing rental fraud based on falsified income statements or employment records.

5. Integrating External Data Verification and Credit Bureau Checks:

Supplementing internal data with external sources enhances the accuracy of applicant verification. This includes:

- Credit Bureau Reports: Assessing credit history and identifying potential red flags.

- Public Records: Verifying information against publicly available data.

- Third-Party Databases: Accessing specialised databases for identity verification and fraud prevention.

- Link Analysis: Detecting connections between seemingly unrelated applications that share common fraudulent elements.

Industry Application: Automotive dealerships can use credit bureau checks and other data sources to effectively assess the creditworthiness of applicants seeking financing.

6. Implementing Real-Time Fraud Scoring Models:

Real-time fraud scoring provides an immediate assessment of risk based on multiple data points:

- IP Geolocation: Identifying applications originating from high-risk locations.

- Device Fingerprinting: Detecting inconsistencies in device characteristics.

- Historical Application Data: Identifying patterns associated with previous fraudulent activity.

Industry Application: Online lenders can utilise real-time scoring to flag high-risk loan applications, enabling immediate intervention.

7. Leveraging Geolocation and Device Fingerprinting Technologies:

These technologies provide valuable insights into the origin and context of applications:

- Geolocation Analysis: Verifying the applicant’s location and flagging anomalies.

- Device Fingerprinting: Identifying unique device characteristics and detecting inconsistencies.

Industry Application: Ride-sharing companies can ensure driver applications originate from valid geographic regions and are associated with legitimate devices.

8. Fostering Industry Collaboration and Knowledge Sharing:

Sharing information and best practices within industry networks is crucial for staying ahead of evolving fraud tactics:

- Fraud Intelligence Sharing: Collaborating with industry peers to share data on emerging fraud trends and known fraudulent profiles.

- Industry Forums and Working Groups: Participating in collaborative initiatives to develop industry-wide best practices.

Industry Application: Retailers can benefit from sharing data on known fraudulent customer profiles and emerging fraud schemes, improving detection rates across the sector.

9. Implementing Enhanced Post-Application Monitoring:

Continuous monitoring after application approval is essential for detecting latent fraud:

- Transaction Monitoring: Tracking financial transactions for suspicious activity.

- Behavioural Monitoring: Observing changes in customer behaviour that may indicate fraud.

Industry Application: Microfinance institutions can monitor loan repayment patterns for anomalies that may signal fraudulent activity.

Conclusion

By strategically implementing these ten key strategies, businesses across all industries can significantly reduce their exposure to application fraud. A tailored, industry-specific approach, combined with continuous adaptation to evolving fraud tactics, is essential for maintaining a secure and trustworthy business environment in 2025 and beyond. These strategies are not merely reactive measures but proactive investments in business resilience and long-term success.

Get a demo today

Get a demo of Fortiro’s income document verification platform to see how it can help you.