Feb 11, 2025

Fraud in Automotive Lending: A Growing Challenge and How to Address It

Automotive lenders are facing an unprecedented surge in fraud. Recent trends show a link between the increase in fraud cases and economic pressures like rising living costs and interest rates.

Syndicated Fraud is on the Rise

However, opportunistic fraud is just one concern. Individual fraudsters and organised fraud groups are becoming more sophisticated, using technology to their advantage. Automotive lending is a common target as many lenders focus on quick financing.

For example, in late 2024, a criminal syndicate in Australia was charged with a $10 million financing fraud scheme targeting automotive financing companies for vehicles that didn’t exist.

As fraudsters adapt and leverage technology to exploit new vulnerabilities in lending processes, it becomes increasingly challenging for lenders to limit their exposure to fraud during the application process.

An increase in fraud can jeopardise a lender’s financial stability and inflate the cost of borrowing for legitimate customers. Automotive financing teams face pressure from internal and external stakeholders to act against fraud, which can impact their reputation and business growth.

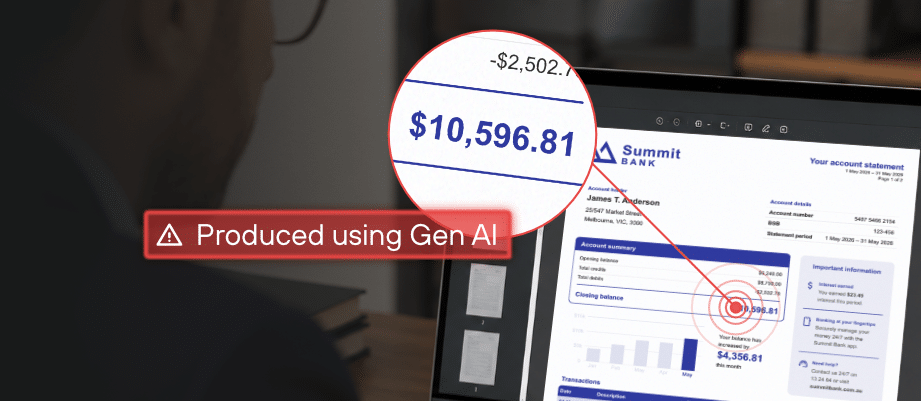

Tampered documents are a key component of car financing fraud. Manipulated payslips, fraudulent invoices, edited bank statements, and falsified supporting documents allow fraudsters to misrepresent their financial stability, employment, or identity to qualify for financing they otherwise wouldn’t receive. These falsified documents appear authentic, making them difficult to detect through manual review alone.

Types of Fraud in Automotive Lending

Numerous types of fraud may occur in automotive lending.

Income Inflation Fraud

Income inflation fraud occurs when individuals alter payslips or other financial documents to inflate their income. As a result, the borrower appears to be more serviceable to lenders, even though the loan remains unaffordable. For example, a borrower with an annual income of $70,000 may falsify their income to reflect $100,000, resulting in a potentially unserviceable loan.

Asset Diversion Fraud

Asset diversion fraud involves acquiring a vehicle via a loan with the intent to resell or disappear with it. Fraudsters often vanish with the asset, leaving lenders to write off substantial losses.

Payment Redirection Fraud

Payment redirection scams happen when fraudsters intercept an invoice, usually by compromising email or pretending to be a legitimate business. They then change the payment details to their own bank account, leaving the original invoice owner unaware. These scams are often very hard to detect. In fact, organised fraud groups carry them out on a large scale using artificial intelligence (AI) and other advanced methods.

Syndicated Fraud

Syndicated fraud is often performed by organised groups that target lenders with well-coordinated schemes. These syndicates often use counterfeit documents, aliases, and templates to exploit vulnerabilities in lenders’ systems. For instance, a single lender may receive multiple applications with slight variations from the same group, bypassing manual detection processes.

Identity Theft Fraud

Identify theft fraud occurs when fraudsters use stolen identities to apply for loans, stealing personal information such as government ID details, driver’s licenses, or other credentials to create fraudulent applications.

Synthetic Identity Fraud

Synthetic identity fraud involves combining real and fake information to create a new, fabricated identity. For example, a fraudster may steal a real person’s information and combine that information with fabricated details to create a new identity.

How Automotive Lenders Can Reduce Risks and Scale Effectively

Lenders need strategies to combat sophisticated fraud without compromising their ability to grow and scale.

Automated Document Fraud Detection Technologies

Automation is revolutionising fraud detection. Machine learning models can analyse large volumes of documents and data to identify anomalies and patterns indicative of fraud.

These systems excel at detecting subtle discrepancies, such as mismatched fonts on invoices, payslips or bank statements, or flag unusual metadata. By automating routine checks, lenders save time and reduce reliance on manual reviews.

Advanced Identity Verification Strategies

Advanced identity verification solutions are important, moving beyond basic checks to incorporate AI-Powered Biometrics, synthetic identity detection, liveness detection and deep fake detection.

Enhance Training for Manual Assessors

While automation is critical, human oversight remains valuable. Training assessors to recognise fraud tactics – such as inconsistencies in document metadata, unexpected fonts, or repetitive templates – can improve detection rates. Teams must be supported by the right tools and technologies to be effective, as document fraud is increasingly hard to detect. This also allows focus on higher-value tasks, such as investigating flagged cases and refining risk models.

Conclusion

Automotive lending fraud is a growing threat that is becoming more challenging due to economic pressures. Lenders must adopt a proactive approach to fraud detection, by leveraging technology and training to stay ahead. By investing in automation, lenders can mitigate risks, reduce costs, and scale their operations effectively. In a landscape where fraud continues to rise, the ability to detect and prevent it at scale will be the defining factor for long-term success.

Read how Pepper Money Asset Finance has benefited from automated fraud detection solutions.

Get a demo today

Get a demo of Fortiro’s income document verification platform to see how it can help you.