Aug 5, 2024

How to Combat Invoice Fraud in Lending and Asset Financing

Invoice fraud is complex.

Fraudsters use invoices in many ways to scam lenders and consumers. In 2023, Australians reported $91.6m in payment redirection scams.

Invoice fraud in asset financing occurs when a borrower or vendor submits false or inflated invoices to secure funding from a lender.

Invoice fraud may be carried out in several ways, including:

- Email compromise, where fraudsters gain unauthorised access to email accounts and the owner is unaware

- Payment redirection scams

- Using false identities and fraudulent invoices

- Creating fake invoices for goods or services not provided

- Vendor and consumer collusion

- Overstating the value of assets

This article discusses these types of invoice fraud, and how Fortiro Protect’s invoice fraud detection can combat them.

Email Compromise

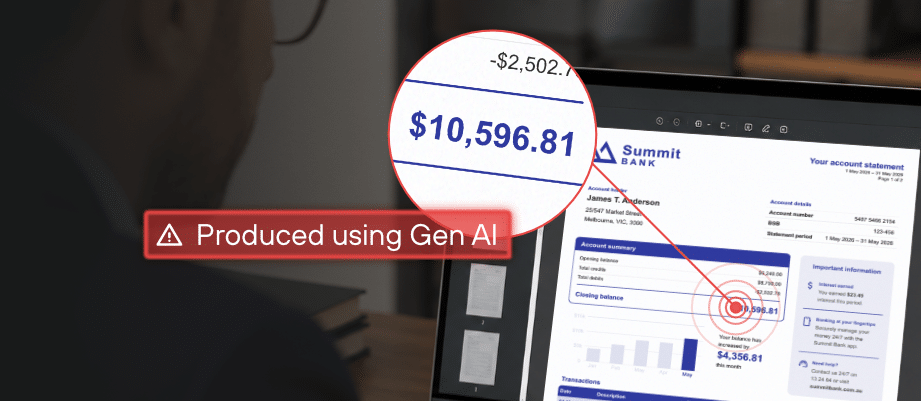

Email compromise involves hacking into or intercepting a borrower’s or lender’s email to access legitimate invoices belonging to borrowers. With this information, fraudsters alter the invoices or create fake ones that seem authentic. The fraudster then sends these invoices to the lender, from a legitimate-looking email, providing new bank account details for payment. As a result, payments intended for legitimate transactions are diverted into the fraudsters’ accounts.

The scam may go undetected until the legitimate supplier asks for the missing payment, revealing that the payments were sent to the fraudsters’ account instead.

A recent case in Sydney saw a hospital scammed out of $2 million. Detectives have noticed an increase in email fraud targeting all members of the community, particularly businesses.

Payment Redirection Scams

Payment redirection scams happen when fraudsters intercept an invoice, usually by compromising email or pretending to be a legitimate business. They then change the payment details to their own bank account, leaving the original invoice owner unaware.

These scams are often very hard to detect. In fact, organised fraud groups carry them out on a large scale using artificial intelligence (AI) and other advanced methods.

In Australia, Bendigo Bank recently intercepted fraudulent invoices that resulted in more than $900,000 in losses by a construction company. These funds were recovered by the bank through their fraud detection and recovery processes.

Identity Fraud + Invoice Fraud

Fraudsters often combine identity fraud and invoice fraud to execute complex schemes that deceive lenders.

Identity fraud involves stealing or fabricating personal information to impersonate others, including obtaining sensitive personal data, identification documents and bank account information.

Invoice fraud involves creating fake invoices or tampering with existing invoices, to extract money from a company or individual. Fraudsters generate fraudulent invoices under false identities.

When used together, these types of fraud can create a more convincing and sophisticated scam, leaving lenders and borrowers vulnerable to losses and write-offs.

For example, a fraudster might steal someone’s identity to create a fake business, and fabricate invoices for non-existent goods or services, ultimately securing loans.

Consumer invoice fraud

Consumers use various tactics involving fraudulent invoices to exploit lenders, such as:

- Fake Invoices

Creating invoices for goods or services that were never provided. These invoices are then submitted to the lender for financing.

- Duplicate Invoices

Submitting the same invoice multiple times to obtain funds from different lenders or repeatedly from the same lender.

- Inflated Invoices

Submitting invoices with higher amounts.

- Collusion

The vendor’s employees collude with consumers to create fraudulent invoices or inflate legitimate ones, splitting the proceeds from the fraud.

The prevalence of these tactics can be influenced by the effectiveness of fraud detection and prevention measures implemented by lenders. Industries with high transaction volumes and complex payment processes – like lending and insurance – may be more susceptible to these types of fraud.

How to combat invoice fraud

Many organisations rely on manual processes to detect invoice fraud. However, manually combating invoice fraud presents several significant challenges:

- Time-Consuming, Labour-Intensive and Prone to Human Error: Manually verifying each invoice for authenticity and accuracy can be extremely time-consuming. It may involve cross-referencing multiple documents, contacting vendors, and checking transaction histories, which can significantly reduce operational efficiency. In addition, manual processes are prone to human error. Mistakes in data entry, poor oversight in verifying details, or misinterpreting information can lead to fraudulent invoices being approved incorrectly.

- Difficulty in Detecting Sophisticated Fraud: Fraudsters often use advanced techniques to create fraudulent invoices that appear legitimate. Manual processes might not be able to detect subtle patterns or anomalies that can be identified using advanced algorithms and machine learning.

Forward-thinking lenders are embracing advanced technologies to fortify their defence. Invoice fraud detection systems like Fortiro Protect, are designed to detect and prevent fraud on many documents, including invoices, before it impacts the bottom line.

How to automate the fraud detection process

Going beyond traditional methods and manual verification, Fortiro Protect automates the fraud detection process, reducing the potential for human error and the need for oversight that can lead to fraudulent payments. By detecting document alterations and cross-checking registry systems, Fortiro Protect ensures that transactions are secure and transparent, reducing the risk of unauthorised alterations.

Key features of Fortiro Protect’s invoice fraud detection solution include:

- Automated Detection of Changes: Fortiro Protect detects and flags suspicious alterations in invoices, alerting users to potential fraud attempts in real-time. Fortiro Protect uses machine learning to highlight anomalies including layout, text and digital property alteration, PDF version changes and image-based tampering.

- Validation of Payment Details: We verify account numbers and Bank State Branch (BSB) codes to authenticate payment destinations, ensuring payments are directed to legitimate recipients.

- Australian Business Number (ABN) and Goods and Services Tax (GST) Verification: Fortiro Protect cross-checks invoices against the ABN registry and GST registration, validating compliance and authenticity of invoiced transactions.

- Asset Verification: Fortiro Protect verifies asset descriptions such as Vehicle Identification Numbers (VIN), which is particularly beneficial for sectors like automotive finance, mitigating risks associated with fraudulent asset purchases.

By integrating innovative technologies and industry best practices, lenders can safeguard their financial operations, uphold trust among stakeholders, and sustain long-term growth.

For more information on Fortiro, click here to book a complimentary consultation.

Get a demo today

Get a demo of Fortiro’s income document verification platform to see how it can help you.