Apr 4, 2025

Perspective: Liar Loans, Responsible Lending and Document Fraud

By Sean Quagliani (CEO and Co-Founder, Fortiro)

The resurgence of concerns about ‘liar loans’ in Australia underscores the critical importance of robust and consistent document verification practices across the lending industry. Responsible lending is not just about compliance. It is about trust, accountability and fairness for consumers.

There has been growing discussion about how widespread liar loans really are and whether more needs to be done to tackle them. Some of the questions being raised are:

- What counts as a liar loan?

- Is Responsible Lending enough to deal with the problem?

- Is “soft fraud” a thing?

- And, is a liar loan OK?

Different views are emerging, and the debate is far from settled.

What is a liar loan?

In Australia, ‘liar loans’ primarily refer to mortgages where the borrower has understated their expenses and/or overstated their income amount/type.

Based on my conversations and the recent press coverage on this topic, lenders acknowledge the risk of these loans. There seems to be general acceptance that higher standards and the use of advanced technology are important to combat this risk. There also seems to be heightened scrutiny from ASIC, driving further awareness.

With over $2.3 trillion in outstanding mortgage debt in the Australian market alone, the focus on affordability verification is more important than ever.

Just how pervasive is liar lending?

Liar lending is difficult to quantify, but we know that where there is financial pressure, opportunity, and rationalisation, there are ideal conditions for fraud, including liar lending.

As Comprehensive Credit Reporting (CCR) and transaction analysis (Screen Scraping or Open Banking) continue to evolve, income remains the hot focus. As some variables in the serviceability equation become fixed (such as CCR fixing the number on liabilities), income remains variable and needs to be closely watched.

Rationalisation

Recent data from a 2025 FICO survey shows that:

- One in three Australians (30%) believe exaggerating income on loan applications is justifiable or common practice. That number grows to 53% among Gen Z (born between 1997-2012).

- A similar pattern applies to mortgages, nearly a third (29%) of Australians believe inflating income on applications is either acceptable or routine, climbing to 52% among Gen Z.

The FICO survey shows a concerning shift in attitudes toward liar lending, which is loan fraud, and a rising acceptance among younger people of misrepresenting their finances to obtain a loan despite the serious financial and legal repercussions.

In the survey report, Corey Smith, senior consultant for decisioning, risk and analytics in Australia for FICO, commented, “Application fraud erodes trust in the financial ecosystem. To combat ‘liar loans’, banks must improve their ability to detect inaccuracies – protecting themselves from bad debt while also preventing customers from committing fraud.”

This is certainly a big tick for ‘rationalisation’.

Financial pressure

Cost of living is a critical focus, as economies recover from inflationary pressures. According to a Finder survey from Australia, the ‘Cost of Living Pressure Gauge’ is sitting at 73% in the ‘Very High’ level. In February 2025:

- 59% of mortgage holders cite mortgage stress as a key financial concern

- 36% of homeowners struggle with mortgage payments

- 28% of Australians say that they can’t handle their finances without a credit card

As cost of living has increased and with wage growth relatively low, pressure has been increasing on serviceability for many prospective borrowers.

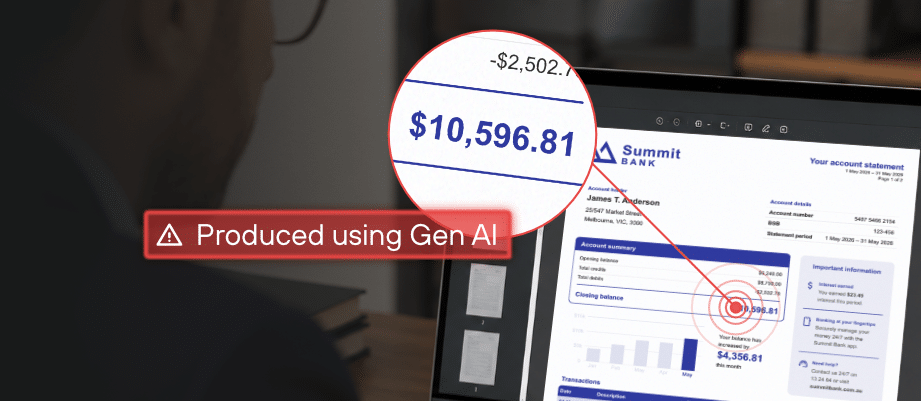

Opportunity: Ease of document manipulation

The ease with which income documents can be tampered with is a critical part of the conversation. In addition to the rapid advancements in generative AI, readily available tools that cost nothing can be used to edit PDF documents and create ‘shallow fake’ images in less than a minute. Bank statement templates can be downloaded for free on a host of websites. Document manipulation is no longer for professional fraudsters.

If you’re interested, I’ve explored this topic in a separate article: four common ways fraudsters create fake income documents.

A global issue

This issue is not just related to Australia. In a recent Equifax analysis, Cherolle Prince from Equifax Canada shared that falsified financials and income are a key driver of mortgage fraud in the Canadian market.

“When we look at some of the reasons behind mortgage fraud, we see that falsified financials and income information is an ongoing major concern,” Prince explained.

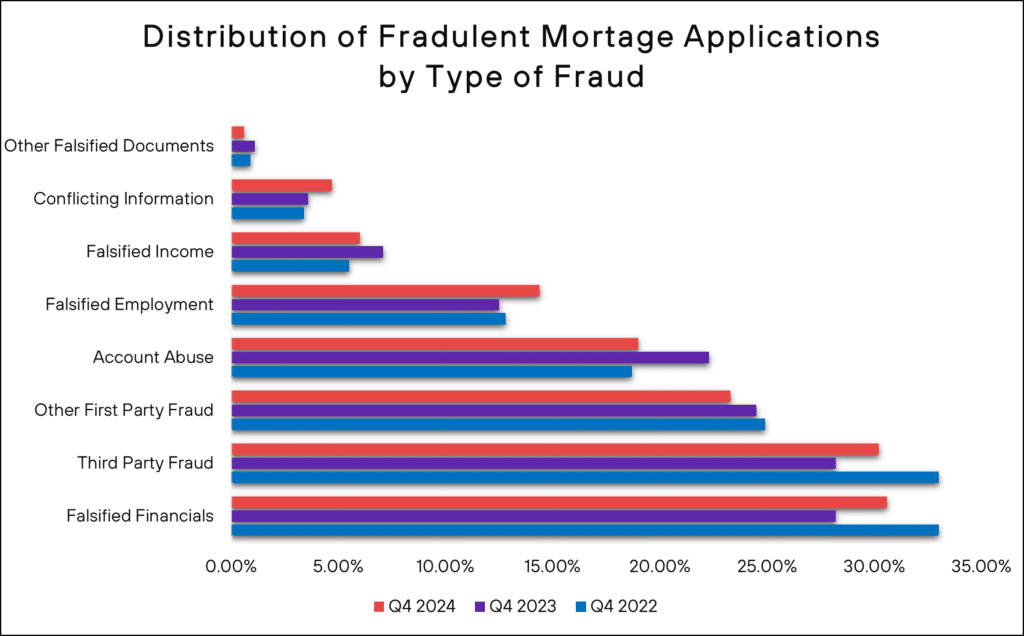

Some highlights from Equifax’s analysis:

- Falsified financials accounted for 30.2% of mortgage fraud cases in Q4 2024, up from 28.2% in Q4 2023.

- Misrepresentation of financial information, where applicants submit fake pay stubs, employment letters, account statements, tax slips, or provide false down payment information, accounts for over 95% of fraudulent applications.

- Other falsified documents made up 23.3% of cases, followed by conflicting information (19.0%) and falsified income (14.4%).

“These findings reinforce our message that lenders need to focus attention on verifying financial documents,” Prince commented.

Affordability document verification is critical

Documents themselves are not the issue. They are convenient, widely adopted across different distribution channels and contain valuable information for fast, accurate decisions. For example, the information in a payslip/pay stub or a tax return is incredibly detailed and critical for an accurate, responsible decision (clarity on base vs. variable income is a simple example).

The problem lies in fraudsters manipulating that information.

This then brings us to the question: Are ‘liar loans’ a problem of Responsible Lending, or fraud?

My take

By definition, fraud is misrepresenting or deceiving to gain an advantage, predominantly financial. In many cases, ‘liar loans’ are good, performing loans. Liar lending fraud is not theft; it is fraud for shelter, and the intent to repay is there.

Despite these good intentions, liar loans are, in my view, fraud. They are difficult to identify because the same fabricated bank statement could be hiding money laundering or hiding liar lending – the techniques used to fabricate the document are the same, and both loans will perform.

Therefore, liar loans are a Responsible Lending problem. Despite a borrower’s best intentions, if a document suggests that financials have been misrepresented, then these particulars must be subject to deeper verification.

Fortiro data

Across retail lending, we typically intercept around 6-7% of income documents as being high risk, with around 50% of those ending up as fraud, and 50% requiring borrower clarification or re-assessment (ie. progresses but it changes somehow, such as a limit change or PAYG becoming self-employed).

6% may sound small to some, but for context, some lenders today would pick up less than 0.14% of this same confirmed fraud – a 2,500%+ increase!

Summary

Fraud prevention is an ecosystem challenge that requires as much collective intelligence as possible, along with multiple capabilities and defences—everything from application-oriented checks such as identity verification to document verification and intermediary risk management. Those who don’t invest in these capabilities will become targets for fraud.

Fortiro’s contribution to this fight is in financial document verification, using accurate, advanced technologies and a combination of patterns to create a powerful network effect.

If you’re a lender and you’re not investing in this area, my advice would be to seriously consider doing so. Reach out, run a pilot and determine if this is a risk for you.

By adopting modern capabilities, lenders can reduce this fraud risk, speed up customer decisions and improve compliance. Our customers report significant savings in fraud losses, by picking up fraudulent applications that otherwise would be approved.

Stronger affordability verification means stronger financial institutions and reinforced confidence in Australia’s lending ecosystem.

About Sean Quagliani

Sean is a Co-founder and the CEO of Fortiro, an Australian technology company that automates financial document reviews and fraud detection. Fortiro’s customers form a powerful network of lenders, insurers, and payment processors, including 3 of the big 4 Australian banks.

Sean is passionate about fraud prevention and has a background in technology, fraud, and cybersecurity.

Get a demo today

Get a demo of Fortiro’s income document verification platform to see how it can help you.