Jun 16, 2026

Five Things Financial Institutions Need to Know about the New US Financial Integrity Laws

The new US Executive Order, Restoring Integrity to America’s Financial System indicates a sharper regulatory focus on the evidence financial institutions rely on to identify customers, assess risk and detect financial crime.

For banks, lenders, fintechs and other regulated institutions, the key shift is clear: customer due diligence is becoming more evidence-led.

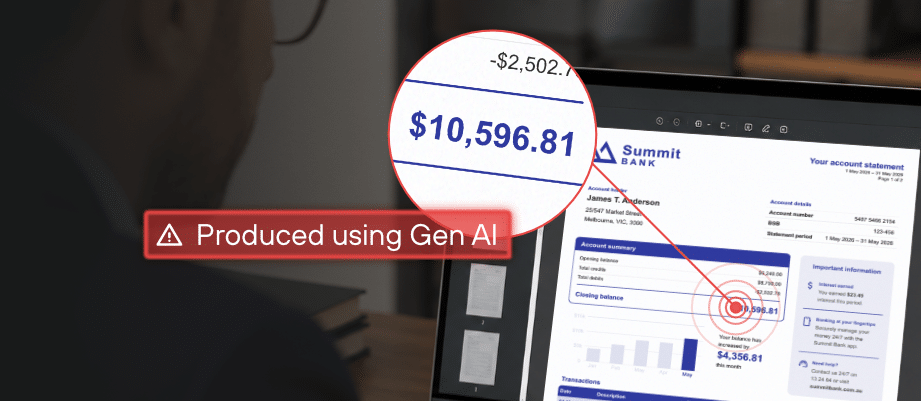

It will no longer be enough to collect identity, income or business documents and move them through the process. Institutions will increasingly need to show that the documents are authentic, the customer story is consistent, and the risk decision can be explained. That matters because document fraud is no longer a marginal issue.

Fortiro’s data shows the scale of the problem is rising sharply. The company has identified millions of high-risk and fraudulent documents across customer workflows and is helping prevent hundreds of millions of dollars in fraud losses every month through automated fraud detection.

Here are Five Things Financial Institutions Need to Know about the Potential Impact of these Changes

1. This is about more than immigration status

Much of the political attention has focused on immigration and work authorisation. But for financial institutions, the practical implications are broader.

The Executive Order directs Treasury, the Consumer Financial Protection Bureau (CFPB) and federal financial regulators to strengthen customer identification, Customer Due Diligence (CDD) and suspicious activity controls. It also flags risks linked to nominee accounts, shell companies, payroll tax evasion, off-the-books payments, unregistered money services businesses, labour trafficking and the use of ITINs in higher-risk account or credit scenarios.

That places this under the umbrella of Anti-Money Laundering, beyond simply an identity issue. The real question for financial institutions is whether they can identify when documents, account structures or payment patterns are being used to disguise the true customer, true source of funds or true nature of activity.

2. Customer due diligence is becoming more evidence-led

The order points to a more demanding version of risk-based due diligence.

Treasury has been directed to propose changes to Bank Secrecy Act regulations to strengthen Customer Due Diligence (CDD) requirements. Those changes are expected to focus on whether institutions collect and verify enough customer identity information to identify nominal and beneficial owners and assess risks linked to illicit finance, sanctions evasion, fraud and other unlawful activity.

This is where the burden shifts: institutions may need to show not only that they collected the required information, but that they validated the reliability of that information when risk indicators were present.

A customer file that includes a pay stub, bank statement, business record or identity document may look complete. But if those documents have been manipulated, generated, borrowed or used to support a false customer profile, the CDD process is compromised from the start.

Fortiro is seeing this shift in real time. Fraudulent documents are becoming more sophisticated, more accessible, and harder for frontline teams to detect manually. The issue is no longer individual instances of fraud which leave evidence of errors. Fraudsters are using scalable and better templates, AI-assisted tools and image manipulation techniques to create documents that look convincing but still contain detectable forensic signals of alteration.

That is why document integrity is becoming central to modern CDD.

3. Anti-money laundering (AML) teams need better document-level risk signals

Financial crime does not always announce itself through a suspicious transaction. Sometimes the first warning sign appears much earlier, in the documents used to open an account, apply for credit or verify income.

The Executive Order specifically calls for red flags related to suspicious payroll activity, funnel structures, nominee accounts, shell companies, off-the-books wage payments and labour trafficking. These risks often relate to false or misleading documentary evidence.

A manipulated bank statement can support a synthetic identity. A false pay stub can disguise unlawful employment arrangements. A fake employer letter can support a credit application. A business document can obscure beneficial ownership or make a shell structure appear legitimate.

Fortiro’s data reinforces the scale of the challenge. Document fraud is not an occasional exception. It is becoming a repeatable, scalable input into financial crime and credit fraud.

For AML teams, the lesson is simple: document fraud is not just a fraud operations problem. It can be an early indicator of money laundering, sanctions evasion, identity misrepresentation or broader criminal activity.

4. Credit risk and AML risk are now more closely connected

The Executive Order also asks regulators to consider the credit risk posed by lending where a borrower may not have valid work authorisation. The legal update notes that the CFPB has been directed to consider clarifying whether potential loss of wages due to deportation could affect a borrower’s ability to repay.

This needs careful handling. Institutions will still need to comply with fair lending laws and avoid blunt, discriminatory or poorly evidenced decision-making. But the broader point is important. Credit risk and AML risk often rely on the same evidence.

Income documents, account statements, employment details, tax records, identity documents and source-of-funds information are used to support both lending decisions and financial crime controls. If those documents are false, both decisions are weakened. That makes document authentication a shared control across credit, fraud, onboarding and AML.

5. Fortiro’s view: stronger CDD starts with stronger evidence verification

For Fortiro, the key message is that financial institutions need to strengthen the evidence verification layer of compliance.

Customer Due Diligence, Carriage and Insurance Paid (CIP) and Anti-Money Laundering monitoring all depend on the quality of customer evidence. If false documents enter the process early, they can contaminate every downstream decision.

That is why Fortiro’s automated document and image fraud detection forms a key part of a modern financial crime control framework. Fortiro helps institutions detect signs of document and image manipulation before those documents are relied on for onboarding, lending or AML decisions. This includes identifying content-, metadata-, forensic- and appearance-based signals that are unable to be identified by humans or metadata-based checks alone.

Just as importantly, Fortiro provides explainable evidence. Compliance and fraud teams need to know what was detected, why it matters and how it should be escalated. A simple pass or fail is not enough in a more evidence-led regulatory environment.

The institutions best placed to respond will be those that can connect document-level risk signals to broader CDD, AML and credit workflows. That means moving beyond document collection and toward document authentication.

The bottom line

The new US direction is still unfolding, but the signal is clear. Financial institutions are likely to be expected to know more about their customers, verify more of the evidence they rely on and explain more of the decisions they make.

At the same time, the fraud environment is intensifying. For AML teams, this makes document integrity a front-line issue. A fake document may not just be an application fraud problem. It may be the first visible sign of a higher-risk customer, a hidden beneficial owner, a false income trail or an attempt to move illicit funds through the financial system.

In that environment, stronger CDD starts with stronger evidence.

Get a demo today

Get a demo of Fortiro’s income document verification platform to see how it can help you.